"Memory is an important category of semiconductors, and it accounts for about a third of the semiconductor market. According to WSTS, the global semiconductor memory market share will reach $155.458 billion by 2022, accounting for 25.34 percent of the global semiconductor market. Under a series of preferential policies issued by the Chinese government, the domestic storage industry has been updated and developed, and the domestic substitution is also widely concerned in the storage industry.

On August 17, 2022, in the "2022 China IC Leadership Summit" hosted by AspenCore, Chen Lei, deputy general manager of Dongxin Semiconductor Co., Ltd. made an analysis of the current situation and future of domestic storage in the title of "Opening the Era of Core, Local storage" core "mission.

Current situation analysis of global storage market

Led by the strong demand in the semiconductor market, the global semiconductor market in 2021 experienced rapid growth. According to WSTS statistics, global semiconductor sales in 2021 reached 555.9 billion US dollars, up 26.2% year on year. China remained the largest semiconductor market, with sales totaling $192.5 billion, up 27.1 percent year on year.

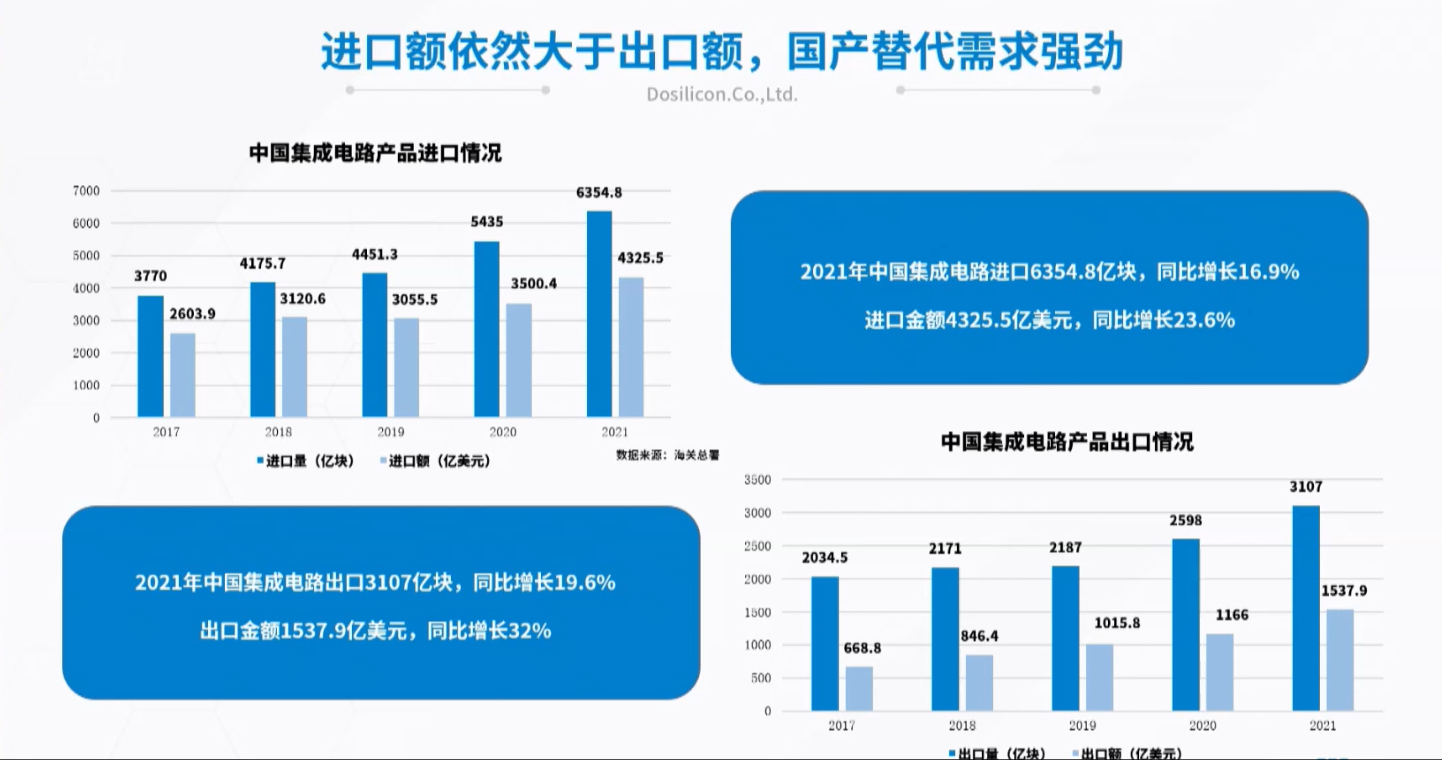

In 2021, China imported 635.48 billion pieces of integrated circuits, up 16.9% year on year, and the import amount exceeded 400 billion US dollars, up 23.6% year on year. In 2021, China exported 310.7 billion pieces of integrated circuits, up 19.6% year on year, and the export value was 153.79 billion US dollars, up 32% year on year. This group of data reflects that last year, China's import and export of semiconductors both production and sales are booming, but the overall import volume is still greater than the export volume, domestic substitution demand is strong.

Led by the strong demand in the semiconductor market, the global semiconductor market in 2021 experienced rapid growth. According to WSTS statistics, global semiconductor sales in 2021 reached 555.9 billion US dollars, up 26.2% year on year. China remained the largest semiconductor market, with sales totaling $192.5 billion, up 27.1 percent year on year.

In 2021, China imported 635.48 billion pieces of integrated circuits, up 16.9% year on year, and the import amount exceeded 400 billion US dollars, up 23.6% year on year. In 2021, China exported 310.7 billion pieces of integrated circuits, up 19.6% year on year, and the export value was 153.79 billion US dollars, up 32% year on year. This group of data reflects that last year, China's import and export of semiconductors both production and sales are booming, but the overall import volume is still greater than the export volume, domestic substitution demand is strong.

According to the data of China Semiconductor Industry Association (CSIA), the sales volume of China's integrated circuit industry in 2021 exceeded 1 trillion yuan, among which the sales scale of semiconductor design companies accounted for more than 40%, reaching 451.9 billion yuan, with a year-on-year growth of 19.6%. This means that China's IC design industry is leading the development of the semiconductor industry chain.

Policy is driving the rise of domestic substitution

The government is actively guiding the semiconductor industry and has issued a series of preferential policies.

From the Outline of National IC Industry Development Promotion in 2014, and the establishment of the first phase of National IC Industry Investment Fund in the same year, trying to stimulate the vitality and creativity of enterprises, break through the bottleneck of key IC equipment and materials, drive the coordinated and sustainable development of industrial chain, and realize the leap-forward development of IC industry.

In 2015, "Made in China 2025" listed integrated circuit industry as the top 10 strategic development industries, requiring efforts to improve the level of integrated circuit design, break through the national information and network security and electronic machine industry development of the core general chip, improve the application of domestic chips.

In 2017, the second phase of the National Integrated Circuit Industry Investment Fund was established to focus on national strategies and emerging industries, and further promote investment and financing to form a synergy with industrial development.

In 2020, the Circular on Policies to Promote High-quality Development of the Integrated Circuit Industry and Software Industry in the New Era formulated and issued fiscal measures in eight areas, including taxation, investment and financing, research and development, import and export, human resources, intellectual property rights, market applications, and international cooperation.

With the support of these policy priorities, domestic substitution has been pushed to a prominent position.

Demand for storage in emerging areas is high

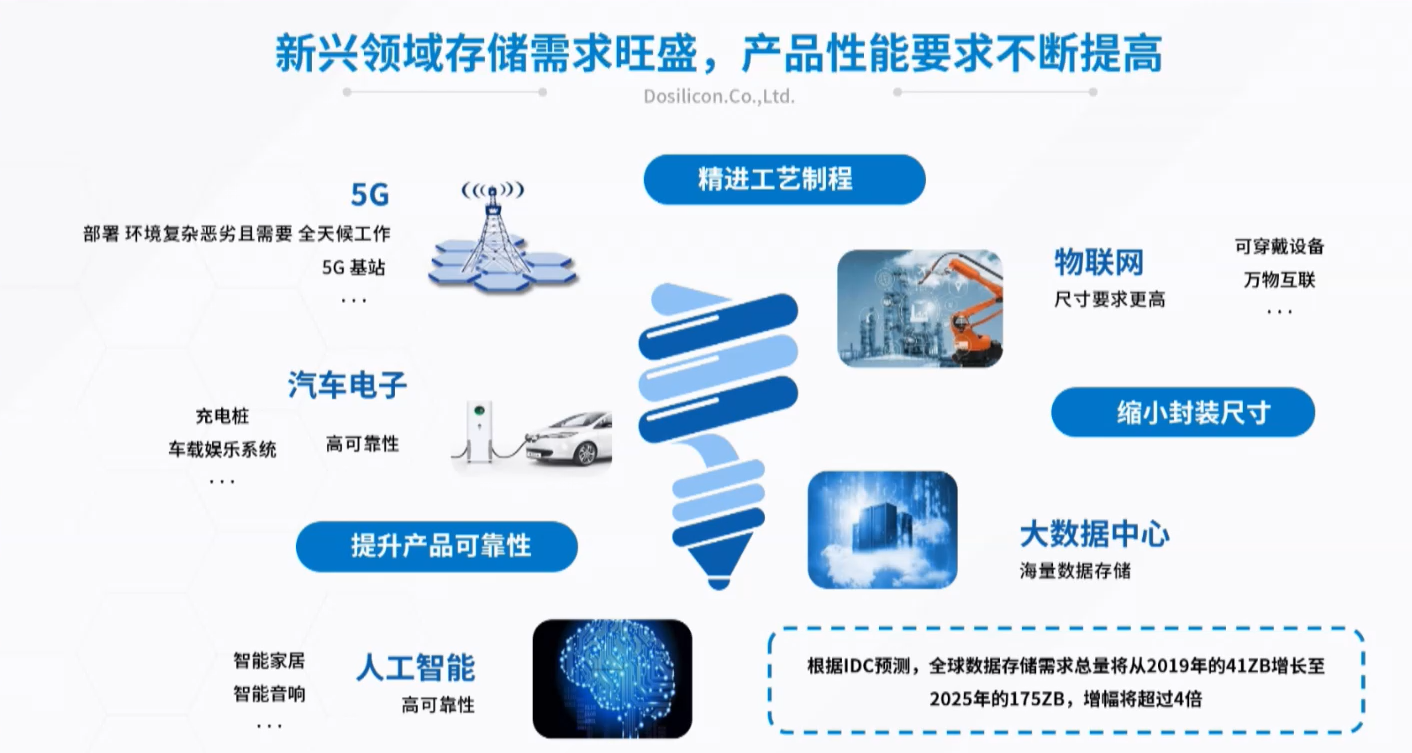

Memory is an important category of semiconductors, with the former accounting for about one-third of the latter's market share. According to WSTS, by 2022, the global semiconductor memory market share will reach $155.458 billion, accounting for 25.34 percent of the global semiconductor market. In addition, IDC forecasts that the total global data storage demand will increase from 41ZB in 2019 to 175ZB in 2025, a more than four-fold increase during the period.

Memory is used most in 3C (computer, communication, consumer electronics) products, which can be subdivided into five markets.

First, 5G base stations. 5G falls into the category of communications, where it works in harsh environments and 24/7. For example, the BBU (baseband processing unit) and AAU (active antenna unit) of a 5G base station are imported with high-performance and highly reliable SLC NAND Flash.

Second, automotive electronics. The dashboards, ADAS, charging piles, V2X and other systems or components of automobiles all require low-capacity memory devices to store data. Currently, NOR Flash and NAND Flash from some storage suppliers have been applied to the automobile gauge market.

Third, the Internet of Things. In recent years, the Internet of Things has a great demand for small capacity memory. In addition to the Internet of Things MCU, with the rise of the wearable market, Bluetooth headset, smart bracelet/watch all have the demand for data storage, which promotes the development of NOR Flash and NAND Flash.

Fourth, big data centers. Big data centers use large storage capacity to store massive amounts of data.

Fifth, artificial intelligence. Mass memory is also commonly used in artificial intelligence, and this technology will help advance the development of advanced memory.

Focus on NOR, NAND, and DRAM

Dongxin Semiconductor is a small and medium capacity memory chip R&D and design company with independent intellectual property rights, products covering NAND Flash, NOR Flash, DRAM, MCP. At present, the company focuses on the product line of NOR Flash, NAND Flash, DRAM, is one of the few domestic Fabless enterprises that can provide NOR, NAND, DRAM design process and product solutions at the same time.

Future planning of Dongxin Semiconductor

Then observe the domestic memory supplier information. By contrast, foreign memory suppliers, such as Samsung, SK Hynix, Micron and other large factories, all adopt IDM mode, which is related to their company evolution. They may choose OEM for part of closed test links, but the main production and manufacturing is in their own hands. Due to the short development time of domestic storage industry, many storage enterprises are still in the Fabless stage, including Zhaoyi Innovation, Dongxin Semiconductor, etc.

Focus on NOR, NAND, and DRAM

Dongxin Semiconductor is a small and medium capacity memory chip R&D and design company with independent intellectual property rights, products covering NAND Flash, NOR Flash, DRAM, MCP. At present, the company focuses on the product line of NOR Flash, NAND Flash, DRAM, is one of the few domestic Fabless enterprises that can provide NOR, NAND, DRAM design process and product solutions at the same time.

Eastcore has two main wafer partners - SMIC and Powerchip. With the evolution of SMIC's process, Dongxin can not only provide package delivery, wafer delivery, but also provide customers with customized memory services, providing an average of 2-3 customized product deliveries per year. The two foundries support Dongxin's NOR, NAND and DRAM products.

After the first 65nm NOR Flash in 2015, Dongxin designed the first 50nm wide voltage NOR Flash (Wuhan XMC foundry) in 2017, and 48nm NOR Flash (force crystal integration electronics foundry) in 2018. This year, NOR Flash, a 48nm large-capacity product manufactured by Lijing Electronics Co., LTD., has reached the stage of providing samples to customers.

NAND is Eastchip's largest business. In 2015, Dongxin designed the first SPI NAND Flash (1GB) in China based on the 38nm process of SMIC. In 2017, Dongxin launched the SPI NAND Flash with a capacity of 2GB. Officially designed 24nm PPI NAND Flash (2GB/4GB/8GB) in 2018, and designed the first 19nm SLC NAND Flash in China in October 2021. Chen Lei said that 19nm basically caught up with the international advanced level.

Dongxin's DRAM products are mainly manufactured by Lijing Electronics, including DDR2 (2GB) based on 38nm technology and LPDDR3 based on 38nm/25nm technology, with capacities of 1GB and 2GB respectively, targeting baseband customers and iot module customers. 2021 also saw the design of 25nm LPDDR4X products aimed at customers in the baseband and automotive segments.

Future planning of Dongxin Semiconductor

In 2021, Dongxin Semiconductor achieved a revenue of 1.134 billion yuan and a net profit of 262 million yuan. According to reports, the company has also expanded its R&D team as early as 2021. By the end of 2021, the number of R&D and technical personnel reached 87 people, accounting for 47.28% of the total number of the company, with a year-on-year increase of 29.85%. At the same time, the company has comprehensively upgraded its research and development platform and training system, conducted in-depth research on users' needs, increased the proportion of differentiated customized products, and continuously optimized its product mix, thus improving its high value-added products.

As for the future research and development direction, Chen Lei said, "First of all, 19nm NAND will realize the pursuit of international advanced technology, but also actively develop vehicle gauge products and integrated storage products. The company's SoC NAND, 1G/2G NAND and PPI NAND Flash have made breakthroughs in the automotive rear fitting market. "We are also building a team to actively enter the automotive spec market, including product design, QA and customer service teams. "We have 8-bit ECC technology built into the 24nm and 19nm SPI NAND Flash, as well as a partial patent on the PPI NAND, which enables robust reliability through step-in and multiple erase."

Source: International electronic business Information

Source: International electronic business Information